Hashprice Volatility and Correlation to Bitcoin

In this post, we examine hashprice volatility and hashprice's correlation to Bitcoin's price.

In this post, we examine hashprice volatility and hashprice's correlation to Bitcoin's price.

Cryptocurrency mining is the process of taking electricity (resource), using it to produce a raw commodity (hashing power), which then secures decentralized network in return for monetary rewards (coins).

Hundreds of thousands of individuals around the world are partaking in cryptocurrency mining; contributing hashing power to help power dozens of networks. Miners are by majority, profit-driven. They are burning electricity and providing hashpower with a goal to make money from it.

As such, miners are tied to the value of the underlying hashrate they produce Hashprice. For miners who have been through crypto cycles, they know how volatile this value can be. One month miners are printing cash and doubling down on their expansion plans, the next they will barely be at breakeven and will wonder where their Excel spreadsheet went wrong.

We wanted to do a deep dive on the volatility of crypto mining reward, why we think this is the case, and if it is correlated to other assets.

Been a while since our 1st-year university statistics course, so we thought it would be helpful for a quick refresher. If you are a stats god then you can skip this part.

Volatility is a statistical measure of the dispersion (the size of the distribution of values) of returns for a given asset. The higher the volatility, the riskier the asset. Volatility can be measured as the standard deviation of the change in the price of an asset. Regular volatility is a backwards-looking measurement.

The simplest way to look at volatility is taking the standard deviation, which is the square root of the average variance of the data from its mean. This measure requires the distribution to be normally distributed (symmetric about the mean).

Unfortunately, the returns of investment performance aren’t always normally distributed. They can suffer from skewness, kurtosis and heteroskedasticity. Skewness is when return distributions are asymmetrical, meaning there are many high and low periods of performance. Kurtosis means there is an abnormally large number of positive and/or negative periods of performance. Together they distort the bell-shaped curve of the normal distribution and throw off the accuracy of standard deviation as a measure of risk. Heteroskedasticity is when the variance of the sample size is not constant over time, so standard deviation fluctuates based on the period you look at. If these issues exist it may be better to look at a histogram than only the standard deviation.

Mining profitability depends mostly on three factors.

The first factor that affects miners’ revenue is **network difficulty. **The difficulty\\ \*\*can increase or decrease miners’ profitability by reducing or increasing the number of coins generated per the same amount of hashing power. For Bitcoin, this network difficulty level adjusts every ~2 weeks based on the amount of hashrate on the network.

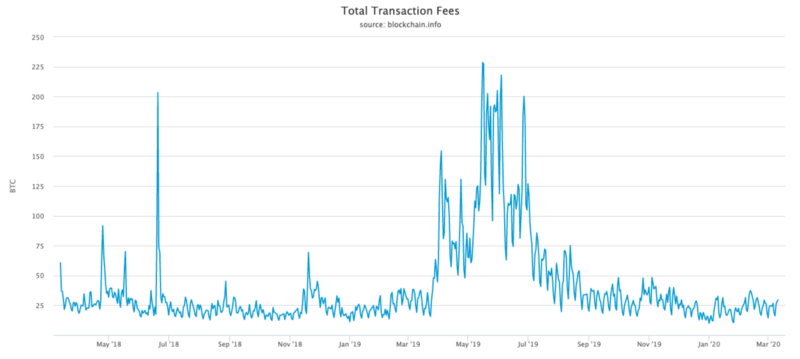

The second factor is the emission rate. The emission rate is the compensation rewarded to miners for solving a block and securing the network. It is a function of the block reward and transaction fees. The block reward simply refers to the new coins distributed by the network to miners for each successfully solved block. In Bitcoin, the miner that successfully finds a block is rewarded 12.5 BTC for their efforts. This number declines over time as we approach the maximum amount of BTC (21 million in 2140). In May-2020 it will decrease to 6.25 BTC per block. Some networks like Bitcoin also have considerable amounts of transactions fees rewarded to miners. These fees are the total of fees paid by users of Bitcoin (to execute transactions). In Dec-2019 this was roughly equal to 3–4% of the block reward.

The last component is the cryptocurrency’s fiat value. Miners’ revenue is denominated in cryptocurrency, therefore, price fluctuations pose a big risk to those who made a big initial investment in mining hardware.

To get the value of hashrate for a given day you can use the following formula:

(User Hashrate (in Hashes per Second) / 2³²) _ ((Daily Emission / Blocks per day) / Network Difficulty) _ Seconds per DayThat will give you a rough estimate on how much a hash of SHA-256 was worth on a given day if used it to mine on the Bitcoin network.

As mentioned above, difficulty adjusts to ensure that blocks are mined at a stable predetermined rate. Bitcoin’s difficulty adjusts every 2016 blocks, which is roughly every 14 days. Most altcoins like Zcash, Ethereum, Horizen, Sia, etc. have a faster difficulty adjustment rate which means that mining rewards are more sensitive to short-term hashrate fluctuations and therefore more volatile.

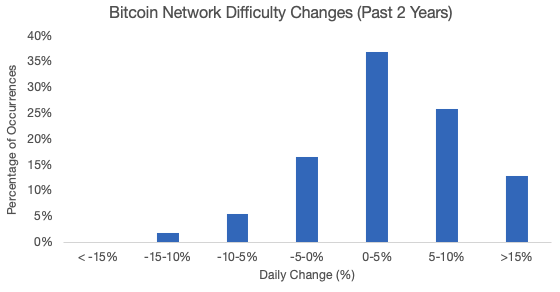

However, this increase in difficulty and consequently decrease in mining revenue hasn’t been smooth. The standard deviation of the difficulty changes was 5.7%.

This means that there’s statistically a 45% chance that the next difficulty adjustment will be larger than a 5.0% (positive or negative). These large swings in difficulty prevent large mining operations from forecasting their mining rewards accurately.

Yet difficulty is only one component of hashprice….

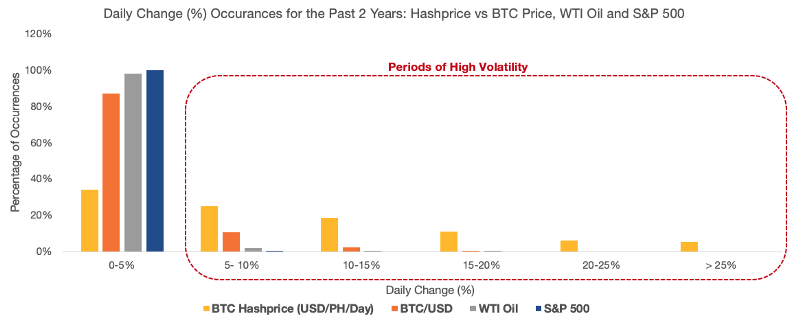

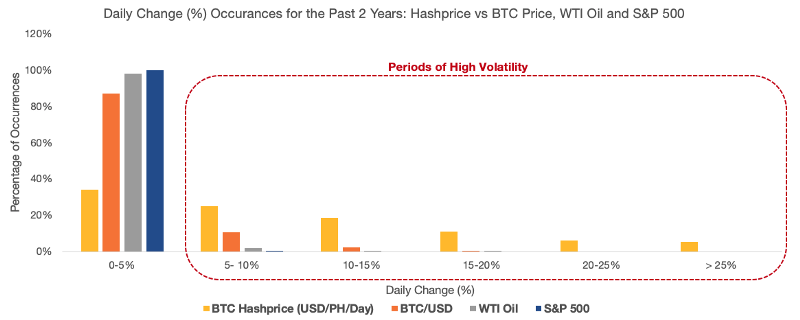

To give context to how volatile hashprice is, we put it up against the price of Bitcoin, WTI Oil and the S&P 500.

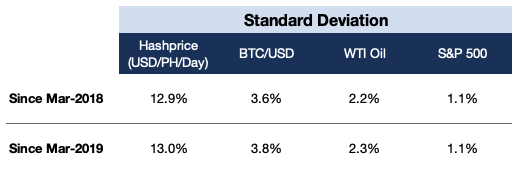

When calculating the standard deviation of returns you realize that hashprice is an incredibly volatile asset. Over the past two years, it has had a standard deviation of ~13%. This is ~3x Bitcoin, ~6x WTI Oil and ~12x the S&P 500.

Given some of the flaws of standard deviation as a measure of risk we also wanted to build the analysis out as a histogram of returns. As you can see from the below, WTI Oil and S&P 500 will rarely have a daily change greater than 5%. Bitcoin is more volatile and it isn’t uncommon for days of 15% changes. However, hashprice is by far the most volatile with daily changes extending out over 25%.

To understand why hashprice is so volatile we must go back to looking at it as a function of network difficulty, emission rate and Bitcoin price.

As we determined earlier network difficulty is very volatile. Every 2 weeks it adjusts based on the hashrate of the network. What we have observed over time is that network hashrate increases. This is largely due to new technologic innovations (i.e. new chip technology) as well as more machines added onto the network. However day-to-day hashrate is extremely hard to predict. It is affected by macro events like the Sichuan province length, Bitcoin prices, other production costs, deployment of new machines etc.

The next component to look at is the emission rate. This is made up of the block reward and transaction fees. Block rewards stay constant for ~4 year periods, so that isn’t a cause for the high volatility over the period we looked at. However, transaction fees are quite volatile. On a daily basis, these are jumping around based on the number of transactions on the Bitcoin network.

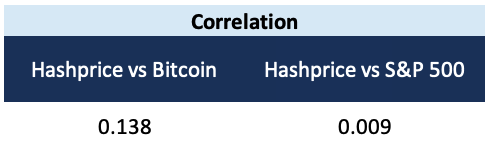

The correlation coefficient is a measure of the strength of the relationship between the relative movements of two assets. It is used to determine if two assets have some form of dependency. If the correlation coefficient of two assets is 0, it means that there is no linear relationship between them. When the value of it is small (between -0.1 and +0.1), the assets have a very weak linear relationship.

Running the correlation between hashprice vs Bitcoin we can see a very weak relationship. That is because bitcoin price is one of a few factors that affect hashprice. We also can determine there is no significant correlation between hashprice and the equity markets.

The analysis above highlights why financial instruments are so important for miners. Hashprice is extremely volatile, and miners take the full brunt of this in the current system. The ability to transfer risk will aide miners greatly in a quest to build stable, long-term businesses.

We think hashrate is an incredibly interesting asset that is based on many strong macro fundamental factors. The fundamental component mixed with the volatility will make it an attractive asset class for traders to engage with.

Join the newsletter to receive the latest updates in your inbox.

Every ASIC ships from the factory with more voltage than necessary. AutoTuner claws it back.

A debugging journey through Zcash mining, the Stratum protocol, and the gap between spec sheet and actual machine behaviour.

{kind=link}